Digitization in Mechanical Engineering

Despite record sales in German systems and mechanical engineering the growth prospects in the core business are moderate. New solution approaches are needed to counteract this trend. With the development of an innovative, digital products and service business the growth limits can be shattered. A successful establishment of the digital business promises to be no less than the renaissance of systems and mechanical engineering.

Beyond the limits of growth

It is the case with growth forecasts: The simpler the justification, the more suspicious one should be. For example, the British economist Thomas Malthus had this experience when he warned of wars and famines in Europe at the end of the 18th century. His reasoning: While the population was growing exponentially, food production was only experiencing linear growth. He quickly realised that this situation would sooner or later lead to a collapse, the so-called “Malthusian nightmare”. However, the catastrophe never came to pass because Malthus could not even begin to imagine the productivity gains that would eventually accelerate agriculture. From today’s point of view, Malthus presents a sad figure: a grumpy killjoy who lacked imagination and optimism as well as belief in the innovative potential of humanity.

No dynamic growth in core business in sight

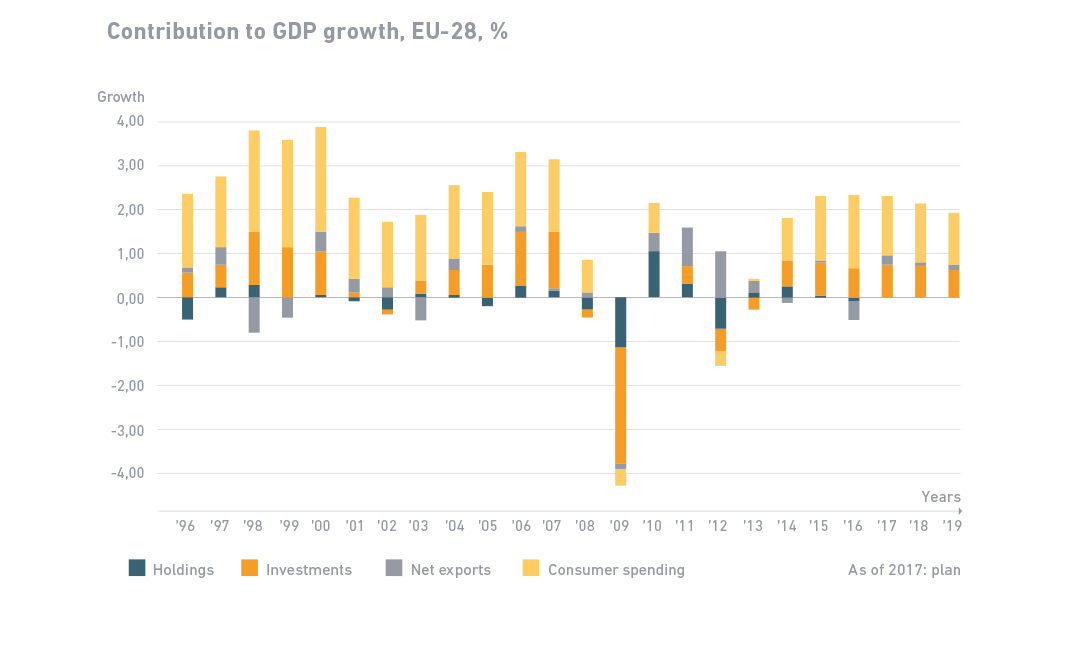

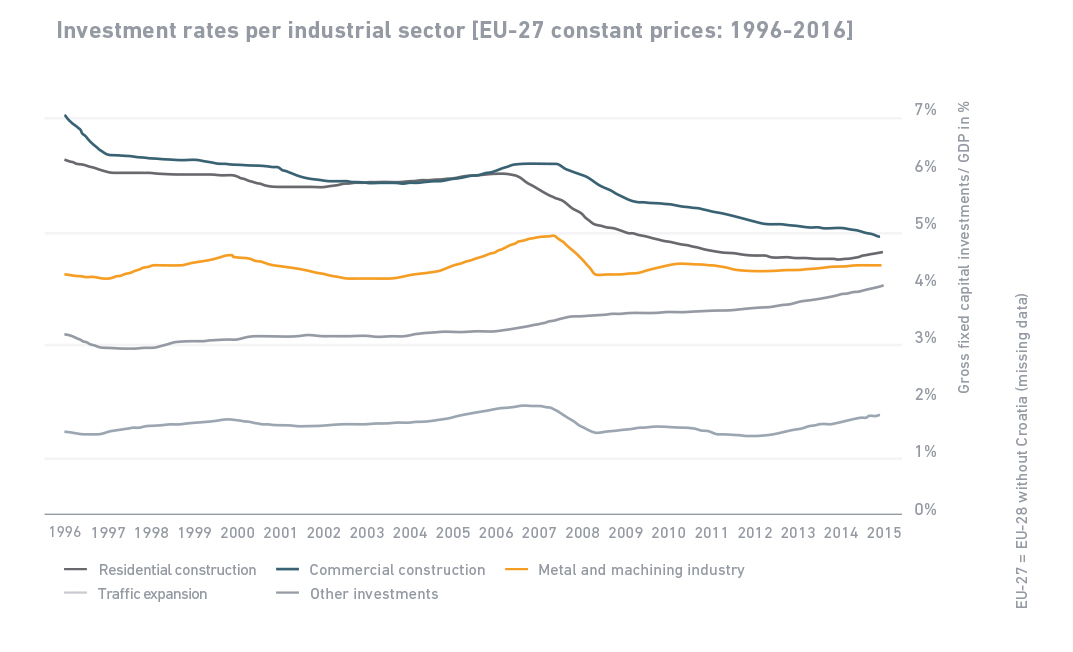

Actually, European mechanical and systems engineering is doing well. In recent years, the industry has achieved average growth of 1.4% in its core business in Europe. Even though growth has increased in 2017 and the forecast promises further growth in 2018, the momentum of the core business is low and a persisting investment rate is inhibiting growth prospects. Gloomy prophecies and anxious admonishers do not quite fit into the picture in the face of steady growth – nobody needs a new Malthus. However, one of the more complex truths is that this snapshot cannot hide the longer-term industry trends that are a cause for concern: For example, consumer spending has long been the driver of GDP growth rather than investment in Europe. The latter have dropped off in the last decade and are still below the long-term average (cf. Fig. 1). In Europe, a decoupling of GDP growth from investment can be observed. Investment rates for mechanical engineering, on the other hand, show a steady decline over the years in terms of gross domestic product. Only the investment rate for intangible investments such as R&D and software (other investments) has grown steadily (cf. Fig. 2).

These long-term developments led to moderate growth in the core business of 1.4% in recent years and no market indicator suggests a renaissance of the core business. The preliminary conclusion is thus: The higher growth in European mechanical engineering is nothing more than a snapshot. With low investment rates and no other growth impulses, there is no long-term prospect of any major growth in the core business. And that certainly dampens the mood of European mechanical and plant engineering. Against this background, looking for growth areas should be the order of the day.

The Malthus effect

In his day, Thomas Malthus made the mistake of dramatically underestimating the speed at which technical advances changed food production. Significant increases in productivity enabled significantly more people to be fed than what had previously been possible.

Today’s parallel for Malthus’ mass production and division of labour is digital technologies, such as augmented reality or artificial intelligence, on the basis of which new value-added digital products and services emerge that have the potential to generate new growth beyond the usual revenue mechanisms. The adoption of such technologies helps to more efficiently solve strategic challenges in the manufacturing industry that are beyond the reach of machine and plant manufacturers to physically optimise their products. These include short notice of customer requirements, which are difficult to plan for, short cycles, as well as rising labour costs or protectionist barriers in the formerly low-cost countries, and the increasing variety of products and their variants. The fact that Malthus did not foresee the far-reaching effects of the onset of industrialisation on manufacturing systems can hardly be blamed on him. After all, there were no data or any reliable information from which to deduce the series of technological explosions in food production.

Financial markets show the way

It is hard to blame Malthus for not having seen the far-reaching effects of the emerging industrialization on production systems - after all, there was no data or reliable evidence from which the series of technological explosions in food production could have been derived.

Today, the attractiveness of complementary technology segments can already be analysed on the basis of financial market data: While systems and mechanical engineering has underperformed in the Dow Jones Industrial Average Index since 2008, technology segments of Microsystems Technology and Predictive Analysis Systems have been growing dynamically. The increase in value over the past 3 years was 212% for Microsystems Technology and 132% for Predictive Analysis Systems, while only 129% was realised in plant and mechanical engineering. Systems and machine manufacturers can benefit from the high corporate value in establishing complementary digital technology business.

The Microsystems Technology technology segment includes manufacturers of sensor and actuator systems. Mechanical and systems engineering is one of five key market segments for the industry. The Microsystems Technology is characterised by a high innovation rate and the development moving towards cognitive sensors that allow a relief of the operator and the introduction of sensor-based assistance functions. Over the past three years, the analysed companies benefited from dynamic sales growth of 15% on average and a high valuation of 20.6 TEV/EBITDA multiple. The Technology Segment Predictive Analysis Systems is based on Deep Technology Machine Learning (ML). Machine learning refers to the generation of knowledge from experience: artificial systems learn from examples and can generalise these after completion of the learning phase. Machine learning was first used in marketing optimisation (analysis of propensity to buy) and in the financial industry (fraud detection). In mechanical and plant engineering, machine learning is rapidly spreading in applications such as predictive maintenance and predictive quality.

Over the past three years, the analysed companies benefited from dynamic sales growth of 30% on average and a high valuation. Compared to the two complementary dynamic technology segments, mechanical and plant engineering developed moderately: Over the past three years, the analysed companies generated sales growth of 1.4% on average and reached a high valuation of 10.2 TEV/EBITDA multiple. The business development in complementary technology segments increases the enterprise value and fuels the growth of machine and systems manufacturers.

Most of these new digital playgrounds are still in an early growth phase, characterised by minimal market structures and an unclear pool of suppliers. The market segments are not yet distributed but there is great momentum in the segments. Anyone not content with observing the proceedings from the sidelines should quickly get down to business - whether alone or as part of a strong ecosystem.

Growth according to the new rules of the game

When the industrial revolution of the early nineteenth century encompassed all of Europe, it meant not only the end of Malthus’ theory, but also a radical change in economic, manufacturing and labour forms.

Digitization is also characterised by market mechanisms that are quite radically different from the usual rules of the game in mechanical engineering. Resolutely entering the digital product and service business therefore means much more than mere expansion of the existing business model with its processes, structures and logic. While mechanical engineers have been successful with their products, above all with niche strategies in homogeneous market segments, thanks to rising economies of scale, a much broader customer target group can be addressed in the digital business. The price, however, is the need to compete against companies in the IT and high-tech environment, which are most well versed in this type of information-based market. To assert oneself against this competition is a considerable challenge for the current global leaders in niche markets but it is also the path to achieving long-term dynamic growth. In the end Malthus was right about one thing: things will end badly if nothing changes.